The shortcomings of the VAT apportionment formula set out in 2011, have been addressed in a new formula which applies with effect from all financial years commencing on or after 1 January 2024. We highlight important adjustments to the formula which is laid out new Binding General ruling, BGR 16 (Issue 3).

Section 17(1) of the Value-Added Tax Act, 1991 (VAT Act) sets out the way in which a VAT vendor may deduct VAT payable in respect of goods or services acquired

partly to make taxable supplies, and

partly for another non-taxable purpose – for example, exempt supplies, private use or other non-taxable purposes. The section provides that such an apportionment must be made according to an apportionment ratio determined by the South African Revenue Service (SARS) in terms of a ruling contemplated under the Tax Administration Act, 2011 (a binding general ruling or BGR) or a ruling under section 41B (a VAT class ruling or a VAT ruling) of the VAT Act.

The original formula

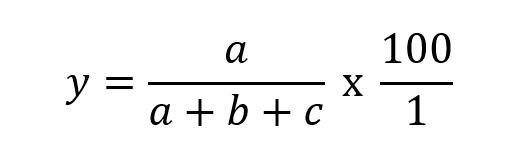

Binding General Ruling 16 (Issue 2) effective from 1 April 2015 was a straightforward, two-page document setting out the so-called standard turnover-based method of apportionment. The apportionment percentage that needed to be applied to VAT incurred on goods and services acquired only partly to make taxable supplies was required to be determined by applying the following formula:

Where:

“y” = the apportionment ratio/percentage;

“a” = the value of all taxable supplies (including deemed taxable supplies) made during the period;

“b” = the value of all exempt supplies made during the period; and

“c” = the sum of

any other amounts not included in “a” or “b” in the formula, which were

received, or which accrued during the period (whether in respect of a supply or not).

Due to many imperfections, the application of the formula in its present formulation gives rise to unfair or unreasonable outcomes in certain circumstances. Therefore, numerous deviations from the prescribed apportionment determination were often sought from SARS. Cognisant of the shortcomings of the formula as provided for in BGR 16 (Issue 2), SARS embarked on a thorough review thereof, which included numerous discussions with stakeholders.

The result is BGR 16 (Issue 3), which was published on 27 November 2023 and applies with effect from all

financial years commencing on or after 1 January 2024. While BGR 16 (Issue 3) does not change the actual formula, it specifies, in detail, which types of amounts and income should be excluded or specifically included within it. The new formula, or more specifically, the elements of the formula as dealt with in BGR 16 (Issue 3), are to be welcomed as they deal with the numerous unresolved issues that arose under the formulation of the formula in BGR 16 (Issue 2).

Why is the new apportionment formula as provided for in BGR 16 (Issue 3) so important for business?

In the first instance, "c" in the formula - that is included in the denominator of the formula - includes the sum of

any other amounts of income not included in “a” or “b” "which was received or accrued during the period, whether in respect of a supply or not". On a strict application of the law, it was necessary to include, for example, gross interest, gross dividends, share capital receipts and foreign exchange gains and losses in "c", with the resultant reduction in apportionment ratio for the vendor. The treatment of substantial once-off receipts of exempt income is also always problematic.

These issues have all been dealt with in detail in BGR 16 (Issue 3).

So, what changes have been made? In a nutshell, the following adjustments or exclusions will apply from 1 January 2024:

- Foreign exchange differences that do not form part of any hedging activities.

- Accounting entries that do not reflect income received, but rather a re-evaluation.

- Profit share from joint ventures or partnerships.

- Proceeds from the supply of a capital asset (the previous exclusion referred to goods or services of a capital nature).

- Extraordinary income as defined.

- Value of goods/services where input tax was denied under section 17(2), such as motor cars, entertainment, etc.

- Trading in financial assets.

- Capital value of loans.

- The cash value of goods supplied by a financier under an installment credit agreement (ICA).

- The portion of a rental payment relating to the capital value of goods supplied under a rental agreement which is entered into as a mechanism of finance.

- Change-in-use adjustments under sections 18, 18A, 18C and 18D.

- Indemnity payments received.

- Manufactured interest and dividends received by the borrower of a securities lending arrangement.

- Debt securitisation transactions.

- The value of equities, debentures or bonds issued as a manner of raising funds.

- Net interest and the use of proxies where no interest is charged.

- Smoothing of dividend receipts and inclusion of proxy dividends.

Whilst SARS provides detail on each of the above in BGR 16 (Issue 3), and there are numerous important developments, it is important to highlight the following:

Extraordinary income

- SARS defines "extraordinary income" as "non-recurring income received due to exceptional circumstances that are unlikely to be repeated". SARS gives an example of extraordinary income dividends received as a result of a re-organisation or liquidation of a company under sections 44, 46 or 47 of the Income Tax Act.

- In our view, section 42 (asset-for-share transactions) and section 45 (intra-group transactions) of the Income Tax Act could also be viewed as instances where there would be extraordinary income received due to exceptional circumstances that are unlikely to be repeated, such as a corporate restructure.

Interest

Dividends

- SARS argues that dividends received must be included in the "c" in the formula (ie the denominator) to reflect the investment activity by the vendor in respect of the relevant investment, notwithstanding that dividends are not a consideration for any supply made by a vendor.

- There is, thankfully, recognition that the flow of dividends in any one year may totally distort the apportionment formula. SARS has therefore provided, in the first instance, for a three-year moving average of dividends received x (prime rate − JIBAR) that must be included in "c" in the formula.

- The three-year moving average is determined by calculating the average of dividends received during the current financial year and two immediately preceding financial years.

- If a vendor does not receive dividends during the current financial year, a three-year moving average of the three preceding years may be used as proxy.

- If a vendor receives no dividends for at least two out of the three years, a five-year moving average must be used instead of the three-year moving average where dividends were received for at least two of the five years.

- If a vendor has not received dividends for two out of the five years as required above, and the vendor is a holding company charging management fees to its subsidiaries, the vendor must include a value equal to the management fees charged for that financial year in the formula as proxy for dividend income. No three-year moving average will be applied in this instance.

- If a vendor has not received dividends for two out of the five years as required above, and the vendor is not a holding company charging management fees to its subsidiaries, the vendor must approach SARS for an alternative manner of determining a value to be included in the formula that appropriately reflects its investment activities.

General

If an alternative apportionment method has been approved for use by a vendor in a VAT ruling or VAT class ruling and the vendor regards the apportionment formula set out in BGR 16 (Issue 3) to be a fairer and more reasonable basis of apportionment, the vendor or class of vendors may approach SARS to have the VAT ruling or VAT class ruling withdrawn from the financial year commencing on or after 1 January 2024. The withdrawal request must be submitted to

vatrulings@sars.gov.za before the end of the financial year commencing on or after 1 January 2024.

Webber Wentzel regularly assists clients with VAT rulings, and we are well placed to assist clients in this regard as well.